A strategic improvisation. This post is a thesis—a thought experiment on how PayPal could evolve from payment processor into a global financial behemoth: the financial operating system for commerce. It describes what PayPal might build, not what it is building today. It is not investment advice, a product review, or a statement of PayPal’s actual plans.

For years, the market has valued PayPal as a payment processor.

That framing may eventually prove as limiting as viewing Amazon as an online bookstore or AWS as a server rental business.

The question is not whether PayPal can process more payments. The question is whether PayPal can evolve into the financial operating system for global commerce—a platform where consumers, merchants, suppliers, lenders, and investors interact through a single network powered by programmable money.

Some elements of this vision exist in embryonic form today; most of the value described here lies in what comes after the payment clears.

If PayPal executes this vision, its addressable opportunity may be measured in trillions of dollars of commerce infrastructure—not payment processing fees alone.

The Market Sees Payments. The Thesis Sees Infrastructure.

Most people encounter PayPal at checkout.

A customer pays. A merchant receives funds. PayPal collects a fee.

That interaction is real—but it is the entry point, not the destination.

The more valuable asset is the network itself: hundreds of millions of consumers, millions of merchants, global payment flows, wallet infrastructure, risk and identity signals, and—critically—the opportunity to keep economic activity inside the platform after money arrives.

Today, a payment often exits the ecosystem immediately. Proceeds sweep to a bank. Suppliers are paid through separate rails. Treasury, lending, FX, and investment run elsewhere.

The thesis starts with a different premise:

PayPal wins not by processing the payment, but by becoming the place where money lives, moves, grows, and executes business rules after the payment.

Everything that happens after checkout is where the trillion-dollar opportunity begins.

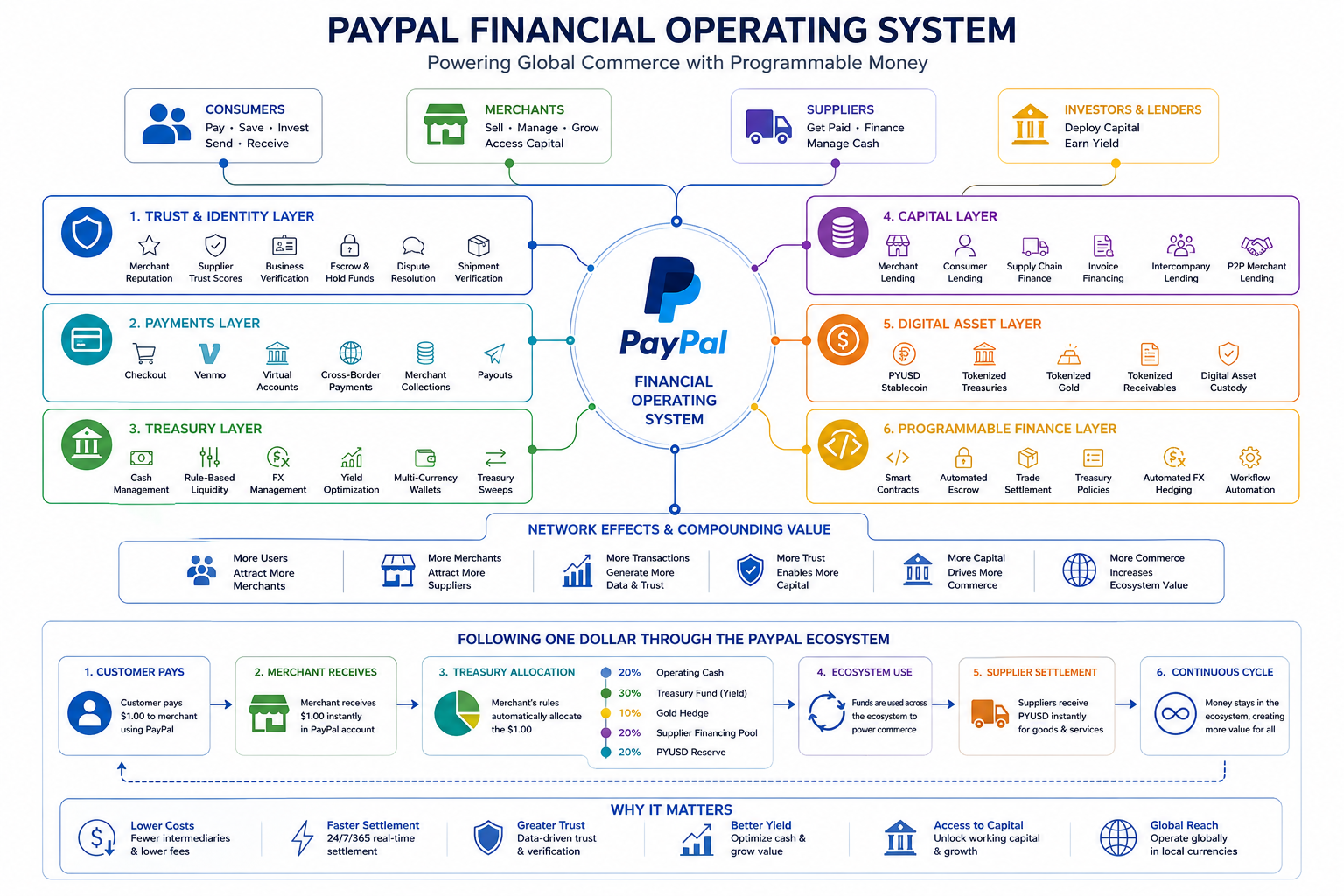

Proposed Ecosystem Overview

A layered model of the financial operating system: trust at the base, payments as the on-ramp, and treasury, capital, digital assets, and programmable finance stacked above.

The layers are intentional. Each one builds on the one below it.

| Layer | Question the platform answers |

|---|---|

| 1. Trust and identity | Can I safely do business with this counterparty? |

| 2. Payments | How does value enter the ecosystem? |

| 3. Treasury | Where does money sit, and how is it allocated? |

| 4. Capital | How is liquidity created, moved, and borrowed? |

| 5. Digital assets | How is value represented on programmable rails? |

| 6. Programmable finance | How are business rules encoded into money itself? |

Payments attract users. Treasury retains balances. Capital creates economic velocity. Digital assets increase flexibility. Programmable finance automates the workflows that today require banks, lawyers, spreadsheets, and manual handoffs.

That stack—not checkout alone—is the financial operating system.

Layer 1: Trust and Identity

Commerce does not begin with payment. It begins with trust.

Imagine sourcing a supplier in India or China. The first question is not how do I pay, but can I trust this supplier to perform.

PayPal sits on a unique asset: transaction history at scale. Over time, the platform could see merchant longevity, refund patterns, chargeback behavior, repeat buyers, dispute rates, and volume trends—and convert that into a portable trust network:

- Supplier reputation scores

- Merchant trust scores

- Verified business identity

- Trade history

- Counterparty risk assessments

Trust becomes measurable. Trust becomes portable. Trust becomes part of the network—just as credit scores became infrastructure for lending, but applied to commerce relationships.

In this vision, PayPal is not only moving money. It is reducing the information asymmetry that makes global trade expensive.

Layer 2: Payments

Payments are the foundation—but only the beginning.

In the full vision, PayPal payment services become the universal on-ramp into the ecosystem:

- Consumer checkout and wallets

- Social and peer-to-peer flows

- Virtual accounts for every customer or invoice

- Cross-border collections

- Stablecoin settlement

Virtual accounts are especially important. Imagine every customer, partner, or invoice receiving a dedicated payment address. The merchant never exposes its primary account. Collections map cleanly to orders. Reconciliation becomes automatic.

Enterprise treasury teams already use this pattern at banks. The thesis extends it to every merchant on the platform—enterprise-grade collection and reconciliation without enterprise-grade complexity.

Payment is the event. Retention is the platform.

Layer 3: Treasury

Most businesses do not struggle to accept money. They struggle to manage it.

Large corporations run treasury management systems with explicit policies. Most small and mid-sized businesses run the same problem inside a checking account—with no rules, no sweeps, no yield, and no automated allocation.

In the thesis, a merchant defines a treasury strategy, not a bank balance:

- Keep $50,000 available for operations

- Sweep excess cash into a Treasury fund

- Hedge 10% against inflation using tokenized gold

- Maintain a payroll reserve for two pay cycles

- Allocate by currency based on supplier concentration

PayPal executes those rules automatically. The merchant stops managing accounts and starts managing policy.

Capabilities in this layer include rule-based liquidity management, treasury sweeps, yield optimization, multi-currency wallets, FX allocation, and automated cash routing—all inside the same platform that processed yesterday’s sales.

This is where SMBs gain access to infrastructure that today belongs only to Fortune 500 treasury departments. That democratization alone could justify a platform valuation far beyond payment processing margins.

Layer 4: Capital

Once balances and transaction history live on the platform, capital becomes network-native.

Today, businesses borrow from banks with underwriting models loosely connected to how they actually operate. In the thesis, the platform sees cash flow, seasonality, counterparties, and repayment capacity in real time.

Imagine a holding company with two subsidiaries: one cash-rich, one capital-constrained. PayPal facilitates intercompany lending—documentation, interest, accounting entries, repayment schedules—automatically.

The same infrastructure extends outward:

- Merchant working capital

- Consumer lending

- Supply-chain finance

- Invoice financing

- Peer-to-peer merchant lending

PayPal becomes more than a payment network. It becomes a capital marketplace—matching liquidity to need inside the same ecosystem where commerce already happens.

The underwriting advantage is structural: the platform sees the business as it runs, not as it reports quarterly.

Layer 5: Digital Assets

Most commentary on PayPal and crypto focuses on PYUSD as a product.

In this thesis, that misses the point.

Stablecoins are infrastructure, not the destination. The question that matters is: what becomes possible when PayPal controls programmable money?

The vision includes:

- PYUSD settlement between counterparties

- Tokenized Treasury Bills

- Tokenized gold

- Tokenized receivables

- Digital asset custody

Businesses diversify reserves without leaving the ecosystem. Consumers access investment products from their wallets. Merchants hedge inflation without opening brokerage accounts.

Digital assets are the flexibility layer—the ability to represent, move, and allocate value on rails that settle in seconds rather than days.

Layer 6: Programmable Finance

This may be the most important layer in the entire thesis.

Traditional money moves when instructed. Programmable money executes business rules.

Imagine purchasing inventory from a supplier. Instead of a wire transfer and a letter of credit, funds deposit into a conditional balance:

- Buyer deposits funds

- Supplier ships goods

- Shipment is verified

- Funds release automatically

The rules are encoded in the transaction itself.

The same pattern applies to treasury sweeps, intercompany lending, revenue sharing, FX hedging, supply-chain finance, and automated accounting. Money behaves like software: conditional, composable, and enforceable without a chain of manual approvals.

Money becomes software.

That is the difference between a payment company and a financial operating system.

Following One Dollar Through the Ecosystem

The thesis is easiest to understand by tracing a single dollar.

A customer pays a merchant. Instead of sweeping to a bank, the dollar enters a PayPal treasury account and is allocated by policy:

Customer payment ($1.00)

│

▼

PayPal Treasury Account

│

├── 20% Operating cash

├── 30% Treasury fund

├── 10% Gold hedge

├── 20% Supplier financing pool

└── 20% PYUSD reserve

That same dollar now:

- Funds daily operations

- Earns yield

- Hedges inflation

- Finances a supplier

- Supports lending

- Settles globally

—all without leaving the PayPal ecosystem.

This is the inflection point where network effects become economic effects. The platform does not merely connect buyer and seller. It activates every dollar that passes through it.

The allocation percentages are illustrative. The principle is not: retained value compounds; exited value does not.

Why Stablecoins Matter

Cross-border commerce is the stress test for this vision.

A merchant in New Jersey paying a supplier in China today may traverse banks, correspondent banks, FX providers, delays, and layered fees—as described in the fragmented world of international rails like SWIFT messaging and correspondent settlement.

In the thesis, the same flow compresses:

Buyer

↓

PYUSD

↓

Supplier

The supplier can hold PYUSD, convert to local currency, invest excess balances, or pay downstream suppliers—still inside the ecosystem.

Stablecoins are not the business. They are the settlement rail that keeps global commerce on-platform instead of leaking back to fragmented banking infrastructure.

Why This Could Be a Trillion-Dollar Outcome

Payment processing is a large business. Platform ownership of commerce infrastructure is a much larger one.

If PayPal remains a processor, its value is tied to transaction volume and take rate. If PayPal becomes the financial operating system—the place where merchants manage treasury, access capital, settle globally, hold digital assets, and encode business rules into money—its value is tied to everything that happens after the payment.

That is a different TAM entirely:

| Processor framing | Operating-system framing |

|---|---|

| Fee on payment volume | Retained balances and treasury AUM |

| Compete on checkout conversion | Compete on ecosystem lock-in |

| Value per transaction | Value per merchant lifetime |

| Replaceable at checkout | Embedded in how the business runs |

Amazon did not become Amazon by selling more books. AWS did not become AWS by renting more servers. PayPal, in this thesis, does not become a trillion-dollar platform by processing more payments.

It gets there by owning the layers above payment.

What Execution Requires

A vision is not a roadmap. Execution would require relentless product build, regulatory navigation, merchant adoption, and trust in automated financial workflows at scale.

The thesis does not assume this is easy. It assumes the prize is large enough to justify the attempt—and that PayPal already holds the two hardest assets: consumer and merchant network density, and a position at the point of commerce.

Whether PayPal chooses to build this stack is a strategic decision. Whether the market is underpricing the opportunity if they do is the argument this post makes.

Conclusion

PayPal is widely understood as a payment processor because payments are what people see.

The trillion-dollar thesis is about what they do not see: the treasury, capital, trust, digital-asset, and programmable-finance layers that could sit on top of the same network.

If PayPal executes this vision, it will not be remembered as a company that moved money from buyer to seller.

It will be remembered as the financial operating system for global commerce—the platform where payments are simply the front door, and everything valuable happens once you are inside.

Payments are the on-ramp. The operating system is the destination.