Most engineers who join a bank from a technology company arrive with a simple mental model:

SWIFT is the system that moves money internationally.

While understandable, that mental model is incomplete.

A more accurate way to think about SWIFT is this:

SWIFT does not move money. SWIFT moves messages.

The actual movement of money happens through correspondent banking relationships, central bank settlement systems, and accounts maintained between financial institutions.

Understanding this distinction is essential for engineers building payment systems, cash management platforms, treasury solutions, liquidity systems, and settlement infrastructure.

The Simplest Mental Model

Think of SWIFT as the diplomatic cable network of global finance.

Governments do not physically move people, equipment, or money through diplomatic cables. Instead, they use secure communication networks to send instructions between embassies, ministries, and governments.

SWIFT serves a similar purpose for banks.

It provides a secure and standardized way for financial institutions to exchange information and instructions.

Banks use SWIFT to communicate:

- Payment instructions

- Settlement instructions

- Cash management reports

- Account statements

- Trade finance messages

- Securities settlement messages

- Foreign exchange confirmations

- Regulatory and compliance information

In other words:

SWIFT is the communication layer of international finance.

Architecture Overview

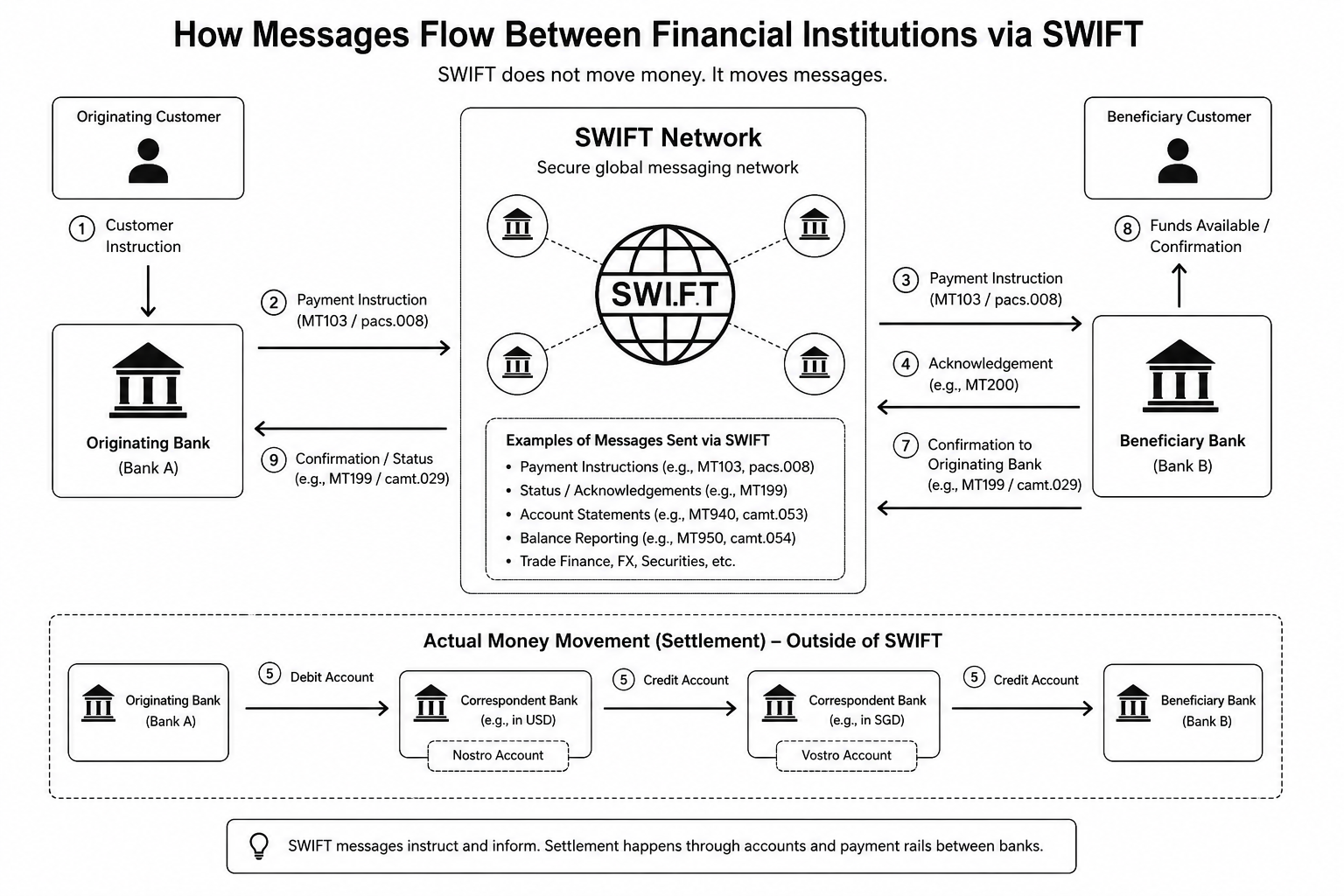

SWIFT carries messages between financial institutions. Actual settlement occurs separately through correspondent banking relationships and settlement systems.

The most important takeaway from this diagram is:

SWIFT is messaging. Settlement is a separate process.

The SWIFT network tells financial institutions what should happen.

Settlement systems ensure that money actually changes ownership.

A Brief History of SWIFT

Before SWIFT existed, banks relied heavily on telex networks to communicate payment instructions.

As international trade expanded during the 1960s and 1970s, telex became increasingly problematic:

- No standard message formats

- High operational risk

- Manual processing

- Frequent interpretation errors

- Limited automation

To solve this problem, a consortium of international banks created SWIFT in 1973.

SWIFT stands for:

Society for Worldwide Interbank Financial Telecommunication

The network became operational in 1977 and gradually replaced telex-based financial communication.

Today, SWIFT connects thousands of financial institutions across more than 200 countries and territories and serves as one of the most important communication networks in the global economy.

Who Owns SWIFT?

Many people assume SWIFT is a government organization.

It is not.

SWIFT is a cooperative organization owned by its member financial institutions.

Its headquarters are located in Belgium.

Because of its critical role in the global financial system, SWIFT is overseen by the National Bank of Belgium in coordination with major central banks around the world.

This governance model reflects SWIFT’s unique position:

- Not a government agency

- Not a commercial bank

- Not a payment network

Instead, it is shared financial infrastructure operated for the benefit of participating institutions.

SWIFT Is Not a Payment Rail

One of the biggest misconceptions among engineers is confusing SWIFT with settlement systems.

Let’s compare them.

| System | Primary Purpose |

|---|---|

| SWIFT | Messaging |

| ACH | Clearing and settlement |

| Fedwire | Real-time gross settlement |

| RTP | Real-time clearing and settlement |

| FedNow | Real-time clearing and settlement |

For a deeper look at the U.S. domestic clearing and settlement rails in this table, see U.S. Domestic Payment Rails and the ACH deep dive. SWIFT sits one layer above these systems: it carries the instruction, while the rails move the money.

When Bank A sends a SWIFT payment message to Bank B:

- A message is transmitted through SWIFT.

- Banks verify and process the instruction.

- Settlement occurs through correspondent accounts or settlement systems.

- Funds become available to the beneficiary.

SWIFT facilitates communication.

It does not hold customer funds.

It does not settle transactions.

It does not maintain account balances for participating banks.

How Banks Are Addressed: BIC

Just as ACH uses routing numbers to identify a destination bank, SWIFT uses the BIC (Business Identifier Code)—commonly called a “SWIFT code”—to address financial institutions on the network.

A BIC is 8 or 11 characters. For example, DEUTDEFF500:

DEUT— institution code (4 characters)DE— country code (2 characters)FF— location code (2 characters)500— branch code (optional, 3 characters)

Here, DEUTDEFF identifies Deutsche Bank in Frankfurt, Germany, and the optional branch suffix targets a specific branch.

The BIC is the addressing layer that sits underneath every payment, statement, and confirmation described below. It is the SWIFT-network equivalent of the routing number in the ACH deep dive—the identifier that tells the network which institution should receive a message.

What Actually Moves the Money?

Suppose a customer in New York sends money to a customer in Singapore.

The originating bank sends a SWIFT payment instruction.

Historically this might have been an MT103 message.

Today it may be an ISO 20022 pacs.008 message.

The message contains information such as:

- Sender

- Beneficiary

- Amount

- Currency

- Routing information

- Remittance information

The actual movement of funds typically occurs through correspondent banking relationships.

Nostro Accounts

A nostro account means:

Our money held at another bank.

Vostro Accounts

A vostro account means:

Your money held at our bank.

The payment instruction travels through SWIFT.

The settlement occurs through these banking relationships.

This distinction is one of the most important concepts for engineers entering financial services.

SWIFT Messages Are Not Just About Payments

Another common misconception is that SWIFT exists solely to support wire transfers.

In reality, SWIFT supports many different business functions.

Payments

Examples include:

- Customer transfers

- Treasury funding transfers

- Bank-to-bank transfers

Cash Management

Banks use SWIFT extensively for account reporting.

Examples include:

- Opening balances

- Closing balances

- Intraday balances

- Transaction activity reports

Many multinational corporations receive account information from dozens or even hundreds of banks using SWIFT.

Trade Finance

Examples include:

- Letters of credit

- Documentary collections

- Bank guarantees

Securities

Examples include:

- Settlement instructions

- Corporate actions

- Custody processing

SWIFT has evolved into a common communication layer used across virtually every major banking business.

Understanding MT Messages

For decades, SWIFT communication relied on MT (Message Type) standards.

Engineers working in legacy banking systems still encounter these formats daily.

Common examples include:

| Message Type | Purpose |

|---|---|

| MT103 | Customer credit transfer |

| MT202 | Financial institution transfer (MT202 COV for cover payments) |

| MT940 | End-of-day customer statement |

| MT942 | Intraday account reporting |

| MT950 | Statement message (booked entries) |

| MT199 | Free-format message |

| MT299 | Free-format bank-to-bank message |

For many years, these messages formed the backbone of international banking communication.

The Migration to ISO 20022

A defining modernization effort in global payments over the past several years has been the migration from MT messages to ISO 20022.

ISO 20022 introduces:

- Richer data structures

- Better standardization

- Improved interoperability

- Enhanced compliance capabilities

- Better straight-through processing

Examples include:

| ISO 20022 Message | Purpose |

|---|---|

| pacs.008 | Customer credit transfer |

| pacs.009 | Financial institution transfer |

| camt.052 | Intraday account reporting |

| camt.053 | End-of-day account statement |

| camt.054 | Debit and credit notifications |

As of late 2025, the coexistence period for cross-border payments ended, and ISO 20022 (the pacs and camt families) is now the baseline for cross-border payment messaging on SWIFT. MT messages still persist in other domains—such as securities (the MT5xx series) and trade finance—so engineers will continue to encounter both formats for years to come.

For engineers building modern payment platforms, understanding ISO 20022 is becoming just as important as understanding SWIFT itself.

SWIFT gpi: Tracking a Cross-Border Payment

Historically, once a bank sent a cross-border payment, it had little visibility into where the payment was or when it would arrive. Correspondent banking is a chain of institutions, and each hop was effectively opaque.

SWIFT gpi (global payments innovation) changed this. Every gpi payment carries a UETR (Unique End-to-End Transaction Reference)—a UUID that lets every bank in the chain report status back to a shared tracker.

For engineers, gpi explains a great deal about how bank payment systems behave:

- Payment status updates arrive asynchronously, as each correspondent confirms its leg of the journey.

- A payment has a lifecycle—initiated, in progress, credited—rather than a single synchronous success or failure.

- Systems correlate updates by UETR, conceptually the same role the trace number plays in the ACH deep dive.

This is why payment platforms inside banks are built around messages and status events rather than synchronous request/response calls.

SWIFT and Sanctions Enforcement

SWIFT also plays a significant role in global financial governance.

Because so much international financial communication passes through the network, SWIFT has become an important mechanism for sanctions enforcement.

Financial institutions connected to SWIFT must comply with sanctions obligations imposed by regulators and governments.

In some cases, sanctioned institutions may lose access to portions of the global financial messaging ecosystem.

This does not make international transactions impossible.

However, it makes participation in global finance substantially more difficult, slower, and more expensive.

As a result, SWIFT has become not only a technical platform but also a strategically important component of international economic policy.

Why Engineers Should Care

Understanding SWIFT helps explain many design decisions found inside banks.

For example:

- Why payment processing is heavily message-driven

- Why payment status updates can arrive asynchronously

- Why settlement and messaging are separate workflows

- Why treasury systems consume account statements

- Why sanctions screening appears throughout payment flows

- Why ISO 20022 modernization projects are happening across the industry

Many banking systems make far more sense once you understand that they are built around financial messages rather than direct movement of money.

Key Takeaways

If you remember only three things about SWIFT, remember these:

- SWIFT does not move money; it moves messages.

- Settlement occurs separately through correspondent banking relationships and settlement systems.

- SWIFT supports much more than payments, including cash management, trade finance, securities processing, and regulatory communication.

The simplest mental model is this:

SWIFT is the secure communication network of international finance.

Just as diplomatic cables allow governments to coordinate activities around the world, SWIFT allows financial institutions to coordinate the movement, reporting, and management of money across borders.